Hurricane Elsa is the first official hurricane of the 2021 season. Last year’s hurricane season produced a record 30 named storms. NOAA’s Climate Prediction Center predicted another above-normal Atlantic hurricane season. The average of all the predictions for the 2021 season is for 17 tropical storms to form, out of which 8 would reach hurricane status.

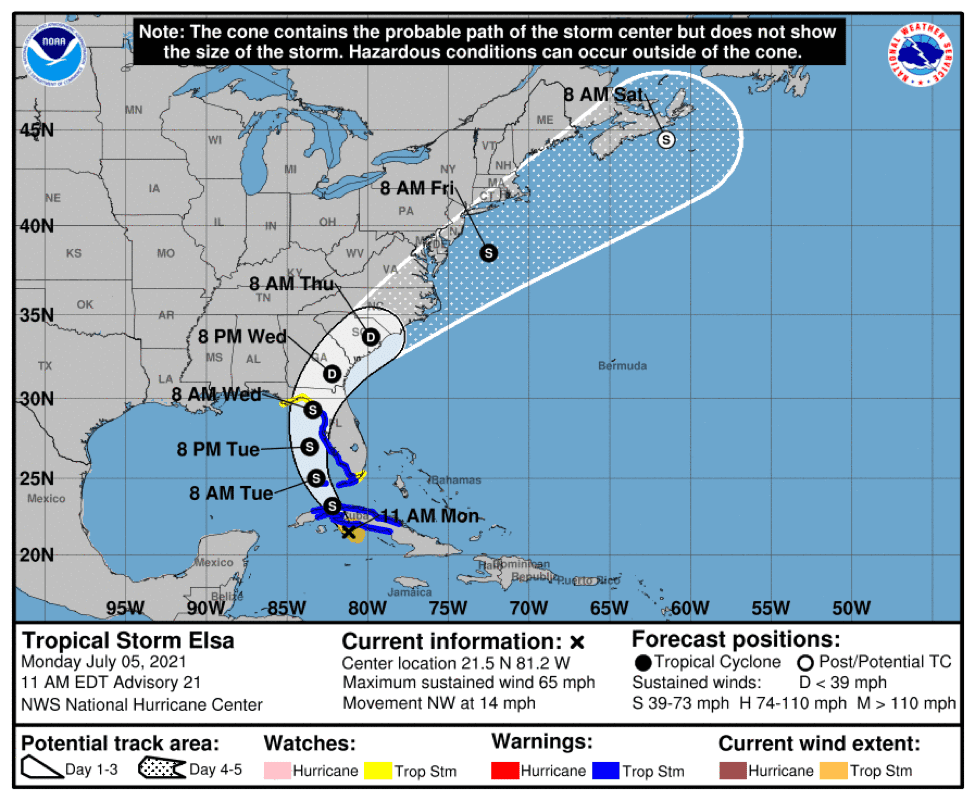

Elsa’s center is now nearing landfall in central Cuba as it continues tracking northwest. Elsa has sustained winds of 65 miles per hour, moving to the northwest at 14 miles per hour and set to cross over Cuba today (July 5).

It should pass over the Florida Keys early Tuesday and then is expected to move near or over portions of the west coast of Florida on Tuesday and Wednesday. Elsa’s track will be influenced by the jet stream near North America and a current area of high pressure over the western Atlantic.

In preparation for the pending storm, Murray + Murray would like to provide some helpful items for policyholders to consider with hurricane claims.

Hurricane Preparedness Tips:

Step One: Prepare for the Storm

For personal safety, identify what storm shelter is available to you and prepare an evacuation plan. Also, make a plan for your pets. Not all emergency shelters will take pets.

Make sure you have bottled water, a first aid kit, flashlights, a battery-powered radio, non-perishable food items, blankets, clothing, prescription drugs, eyeglasses, and personal hygiene supplies. Keep your phone charged and invest in a portable charger.

If you need to evacuate your home, turn off all utilities and disconnect appliances to reduce the chance of additional damage and electrical shock when utilities are restored.

Take proactive steps to protect your property from loss and damage. Install storm shutters or cover windows prior to a hurricane. Be sure there are no loose items around the outside of your home that the wind can carry and cause damages to your property.

Step Two: Take Pictures and Make an Inventory Your Property

Always take photos or videos of your property before a hurricane to properly record the condition of the property. Use your phone to take the pictures and backup the pictures into the cloud.

Take an inventory of your personal property, such as clothes, jewelry, furniture, computers and audio/video equipment. Photos and video of your personal property, as well as sales receipts and the model and the serial numbers of items, will make filing a claim easier. Email yourself a copy of your inventory list and/or store it in a safe location.

Step Three: Gather All Your Important Documents

Gather all important documents such as passports, driver’s licenses, citizenship documents, birth/adoption certificates, insurance policies, etc. and keep them with you or store them electronically. Having access to an electronic copy will help in case your documents are ever misplaced. Download a copy into the cloud and/or email yourself a copy of all your important documents.

Step Four: Review Your Insurance Policy

Review your insurance policy. As you make your preparations, review your insurance policy as it is important to know what your policy covers, what it excludes, and your deductible. Having access to your insurance policy is vitally important before and after a storm. Download and/or email yourself a copy of your entire insurance policy so you have all of the information to review, along with the contact information for your insurance company and your insurance agent.

Step Five: After the Storm Strikes

Stay safe. There may be a lot of damage to your house, property and town’s utilities services. Assess the damage and take photos of everything that is damaged before moving or altering anything on your property. Do not throw away anything that is damaged. Make a list of all items damaged or missing as a result of the hurricane. Save receipts for any cost you incur as a result of the storm, including temporary repairs, debris removal charges or alternative lodging.

Protect your property from further damage (cover broken windows, leaking roofs and damaged walls). Do not make permanent repairs to the property until you file your insurance claim.

File your claim as soon as possible. Call your insurance company and your agent with your policy number and advise them of the damages to your property. You can also file a claim with your insurance company online. Make filing your claim a priority as your policy may require you to file a claim within a certain time frame.

Keep a diary of all conversations and events with the insurance company. Get the names and contact information for each person or adjuster you speak with on your claim. Take detailed notes of all your conversations. Sometimes your insurance company will hire independent contractors to adjust claims. The insurance adjuster works for the insurance company, not for you.

Your insurance company must respond to your communications within 14 days, and it must make a decision about your claim within 90 days of when you file your claim.

If you feel that your insurance company has improperly denied your claim, undervalued your damages, or delayed paying your claim, contact an attorney at Murray + Murray. If you’re not sure whether you’re being treated fairly, or if your insurance company is following the required guidelines and Florida Statutes for handling your claim, Murray + Murray will review your claim for free. We are a Florida insurance claim litigation law firm that holds your insurance company accountable when it violates the duties owed to you, the policyholder.