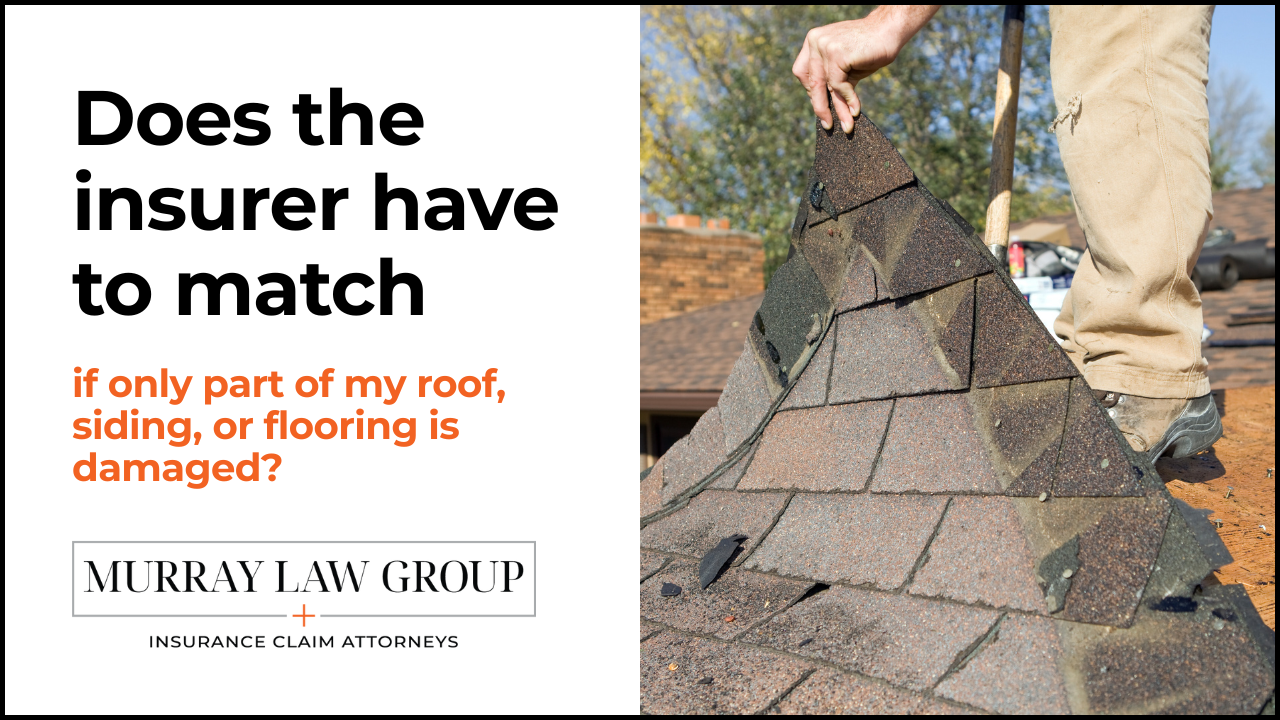

When an insurer agrees to repair only the damaged portion of your roof, siding, or flooring, you may end up with a home that looks like it was repaired in pieces. The real question is whether that result satisfies your policy's requirements — and in many cases, the answer is no.

At Murray Law Group, we regularly see claims where carriers limit their scope to the visibly damaged area, leaving homeowners with a patchwork result and little explanation for why matching was denied.

The Reality Policyholders Need to Understand

Insurance companies routinely write estimates that replace only what is physically broken. It is a cost-driven approach, and it frequently ignores how building materials behave over time — including fading, weathering, and product discontinuation.

When a match cannot be achieved with the remaining undamaged materials, the question of scope becomes a legal one, not just an aesthetic preference.

Why Carriers Push Partial Repairs

Partial repairs cost less. That is the core incentive.

Carriers are not always wrong to limit scope to the damaged area. But they are often wrong to do so without accounting for whether the resulting repair actually restores the property as the policy requires.

The key issue is not whether the repair is functional — it is whether the repair restores the property.

Matching Is a Scope Issue, Not a Style Preference

Homeowners are frequently told that mismatched materials are "cosmetic" and therefore not covered. This framing is often incorrect.

A cosmetic exclusion in a policy applies to specific circumstances defined in that policy. It does not automatically permit a carrier to deliver a repair that visibly fails to restore the property's pre-loss appearance.

When materials cannot reasonably be matched, the proper scope of repair may include replacing a broader section — or in some cases, the entire surface — to achieve a uniform result.

Why This Matters Legally

Florida courts and regulators have addressed matching disputes on multiple occasions. The outcome in any given claim depends on:

- The specific policy language

- The nature and location of the damage

- The availability of matching materials

- The extent of the visual disparity between repaired and unrepaired areas

Four Questions That Determine Whether Matching May Be Owed

Before pushing back on a partial repair estimate, these are the questions that drive the analysis.

1. What does the policy say about replacement and repairs?

The loss settlement provision governs how the insurer is required to restore your property. The exact wording matters, including any limitations the carrier cites to justify a partial repair.

2. Is the original material still available?

If the product has been discontinued, a true match may not be achievable at all. This is one of the strongest factual arguments for broader replacement.

3. How visible is the mismatch?

The more noticeable the disparity between the repaired and unrepaired areas — in color, texture, sheen, or dimension — the harder it is for a carrier to argue the repair restores the home.

4. What documentation supports your position?

Photos, contractor assessments, and supplier availability records can make the difference between a disputed claim and a resolved one.

What to Gather Before You Push Back

If you believe your insurer's estimate is too narrow, the following documentation will strengthen your position:

- Daylight photographs: Full elevation or room-wide shots showing the contrast between repaired and unrepaired areas, plus close-ups of the damaged zone

- Material identifiers: Manufacturer, product line, color name, thickness, and lot numbers where available

- Written confirmation of unavailability: From suppliers or contractors documenting that a matching product cannot be sourced

- The insurer's estimate and any denial language: Keep every version and supplement in the file

Where Claims Commonly Break Down

From a legal and practical standpoint, matching disputes tend to fail at one of these points.

1. The policyholder accepts the cosmetic framing

Once a homeowner accepts that a mismatch is purely cosmetic, the conversation shifts in the carrier's favor. Whether an exclusion actually applies requires a careful reading of policy language — not the adjuster's characterization of it.

2. Documentation is missing or delayed

Matching claims are fact-intensive. Photographs taken before repairs begin, combined with written records showing material unavailability, carry significantly more weight than after-the-fact descriptions.

3. The estimate is accepted without review

Insurance estimates are not final determinations. You have the right to dispute the scope, request a breakdown of any limitations applied, and submit your own contractor's assessment.

What Murray Law Group Advises Clients to Do

1. Read the Loss Settlement Provision Carefully

This is the section of your policy that governs how repairs are to be made. It is one of the most consequential provisions in any homeowners policy and the place to start when evaluating a matching dispute.

2. Do Not Accept "Cosmetic" Characterizations Without Review

Ask the carrier to identify the specific policy language it relies on when calling a mismatch cosmetic. If it cannot point to clear language, that is significant.

3. Document Before Repairs Begin

Once the repair is made, visual evidence of the mismatch is gone. Photograph everything before work starts and throughout the repair process.

4. Get a Contractor Assessment in Writing

A licensed contractor who can confirm that the original material is discontinued — or that a partial repair will result in a visible mismatch — provides the kind of third-party documentation that carries weight in a dispute.

Strategic Insight

Matching disputes are fundamentally about scope.

Insurance companies define scope narrowly because it reduces payments. Your policy may require something broader. The gap between what the carrier estimates and what the policy actually requires is where many claims are won or lost — and where an attorney review can make a material difference.

Ready to Talk About Your Claim?

If your insurer is limiting repairs to the damaged area and leaving your roof, siding, or floors visibly mismatched, you may have grounds to dispute the scope of the estimate.

- Call Murray Law Group: 813-567-5600

- Prefer online? Send a message through our contact form